Battle of the Layer1s: The Zero-Sum Struggle

[ - by MolochNess]

Welcome back, time to delve into the finer details of these ecosystems:

User/Developer experience

Despite periodic surges in adoption, crypto still has a long way to come with regards to user and developer experience.

One of the largest points of friction for normal users: L1s and L2s force user to pay fees in a ‘core token’: $ETH, $ADA, $MATIC, etc. A handful of dapps also require users to use special tokens: Brave, Chainlink, Arweave, The Graph. Even if most of those are business-facing, how many B2B companies charge their clients in speculative and volatile assets? Web3 games use special currencies, ($MANA, $SAND, etc), but at least gamers are accustomed to that.

The status quo works well-enough when most users are crypto die-hards and speculators who would use/hold $ETH regardless. However, average people are unlikely to learn about $ETH and keep re-purchasing it forever simply to pay fees. Users routinely get ‘stuck’ with a wallet full of USDC/NFTs/etc, but not enough $ETH to cover the cost of a transfer or swap, forcing them to embark on a grueling trip to and from Binance. The only way to avoid this is to buy core tokens in excess of what they really need, but that exposes users to volatilty, and most people just don’t want to.

For global adoption to occur, L1s and L2s must enable fees in more mainstream assets (eg: USD stablecoins), or wallets will have to abstract the complexity away from users, swapping assets their users have for the respective core token.

There are various other points of friction, eg: wallet security, or having to sign numerous transactions to accomplish simple tasks, but these are less platform-specific.

Ethereum

The Ethereum user experience varies a lot depending on the layer you interact with.

For Ethereum L1 and EVM L2s/Sidechains, users must hold ETH or MATIC to pay for gas fees. Transaction cost /speed is determined by real-time network demand: popular NFT mints can drive up fees significantly and cause a backlog. App-specific L2s like ImmutableX and dYdX offer fast and gasless transactions, instead charging a % fee on user trades.

As for developers, Solidity and the EVM make it simple for to launch tokens, NFTs, and get into smart contract development. However, despite having a low barrier to entry, it is notoriously difficult to create bulletproof Ethereum contracts. Many $billions have been lost so far to DeFi, NFT, and bridge hacks (1), although not all of that can be attributed to the smart contract model.

Notable EVM contract hacks include:

- October 2021, Cream Finance lost over $130 million, its third hack to date (2).

- April 2022, Beanstalk Finance was hacked for $182 million via a DeFi exploit, when a hacker used a ‘flash loan’ to give themselves majority control over the procotol, and vote to transfer themselves the assets (3).

- April 2022, Aku Dreams NFT project ‘Akutars’ accidentally locked $34 million in their minting contract, rendering it permanently inaccessible (4).

- April 2022, Fei Protocol lost $80 million due to a liquidity pool exploit

- October 2022, Team Finance lost $12 million to an exploit.

- December 2022, the Raydium DEX lost $2 million due to a liquidity pool exploit.

- February 2023, Orion Protocol lost $3 million due to a re-entrancy bug.

- February 2023, BonqDAO and AllianceBlock lost $110 million when a hacker exploited an oracle price feed, minting BEUR to sell on Uniswap (5).

Cardano

The user experience depends mostly on your priorities. Unlike Ethereum, and most EVM chains, Cardano lacks a dynamic fee market that responds to network utilization. This results in lower fees for users, at the cost of not knowing how long transaction confirmation will take. This is better for relaxed payments and trading, but problematic for time-sensitive NFT mints or certain DeFi apps, which might require users to quickly deposit extra collateral to avoid liquidation. There are plans to implement a tiered fee market, where some users pay a ‘base’ fee, while others can pay priority fees to guarantee faster transaction inclusion (6).

One huge upside of the EUTXO model, is deterministic pricing. Users and wallets know the exact cost prior to submitting, which also means transactions can’t randomly fail due to requiring more gas than expected (7).

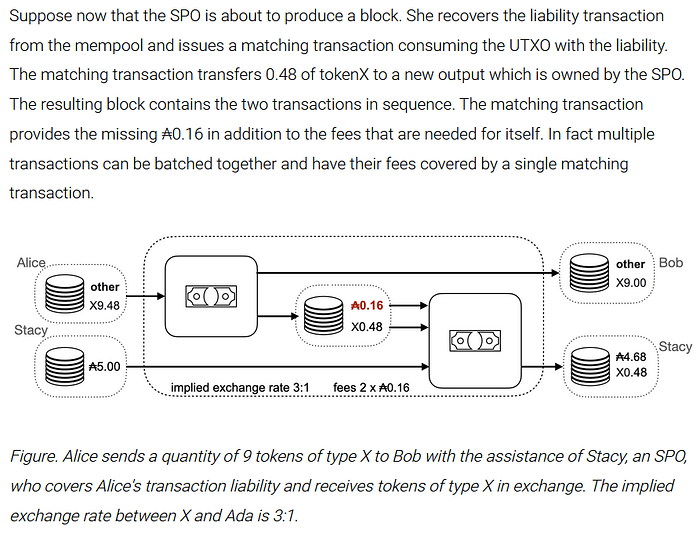

Babel Fees is a proposed upgrade to Cardano, which would allow users to pay for transaction fees in other assets besides $ADA (8). Essentially, Stake Pools opt-into accepting non-$ADA assets for fees, and cover the protocol-level cost (denominated in $ADA) on behalf of users. This would be a massive UX improvement, people could start to use crypto without even realizing it, using familiar currencies (USD, EUR, INR, BRL, etc) to send payments, use DeFi, buy NFTs, and more.

For developers: while it’s easy to create simple tokens and NFTs on Cardano, developing full (L1) dapps remains difficult for average developers, due to the choice of language and ledger model: Plutus (based on Haskell) and the EUTXO model. For some, this is strictly a positive thing: if Solidity/EVM development weren’t so deceptively easy, perhaps $billions in hacks could have been prevented. Beyond Plutus, Marlowe is a domain-specific language (DSL) for financial smart contracts, designed for non-functional developers, or even people with little-to-no coding experience. However, given the relative immaturity of Cardano’s DeFi ecosystem, it remains to be seen how effective Plutus/Marlowe/EUTXO are in preventing smart contract hacks over the long term.

There has also been recent progress in expanding language support on Cardano L1 (9):

- Eopsin, based on Python

- Aiken, based on Rust

- HeliosLang, based on Javascript

- Plu-TS, based on Typescript

- Scalus, based on Scala

Each language compiles down to PlutusCore, the low-level code executed on Cardano L1.

Sidechains and L2s will allow the use of other execution environments (such as EVM, WASM, SVM), allowing developers to pick from a number of options while staying inside the Cardano economy.

IOTA

Like Cardano, IOTA L1 uses the UTXO ledger model. Unlike most blockchains however, there are no elected ‘leaders’ to demand transaction fees from users (‘leaderless consensus’). Instead, access is regulated by ‘Mana’, a resource generated by staking $MIOTA and participating in consensus. Throughput remains scarce though, so many users won’t have enough Mana to cover their needs, so must buy access from 3rd parties or use services that cover the cost for them.

Given the trajectory of Mana research over recent months, it seems like time to put the “feeless” narrative to bed. Earlier Mana designs would allow users to submit transactions at zero cost until a certain threshold of congestion was reached, but this design would leave the network vulnerable to whales, spamming free transactions to create congestion, artificially increasing demand for $MIOTA/Mana. Recent designs allocate a fixed amount of bandwidth, or have a baseline Mana ‘cost’ per transaction. Still, Mana is strictly an upgrade over (superset of) the normal fee model, allowing holders to seamlessly ‘attach’ transactions to the network, while still letting users to buy access from 3rd parties if they don’t wish to hold much $MIOTA. To some this may seem questionable: how is Mana better than staking ETH/ADA and spending rewards on transaction fees, or including your own transactions for free when you get elected to produce a block? Two reasons:

1. In traditional blockchains, unless you rank among the top 100 stakers, you have a miniscule chance of being elected to publish a block at the same time you need to send transactions.

2. Even for users who opt to pay fees, they will get more competitive prices on average, because there isn’t a singular ‘leader’ with a monopoly over transaction inclusion, but tens or hundreds of Mana providers willing to sell access, driving costs down.

Notable Adoption, PoCs and Deployments

Ethereum

The largest dapp and developer ecosystem in crypto, even if you exclude L2s/Sidechains.

- USDT and USDC, each with ~60k daily active users/addresses

- OpenSea: the largest NFT marketplace, with ~80k daily active users/addresses

- Uniswap — the largest decentralized exchange (DEX), with ~50k daily active users/addresses

- Visa has been actively exploring blockchain-based payments on StarkNet, utilizing Account Abstraction to facilitate recurring payments (10).

- Reddit launched ‘Digital Collectibles’ NFTs on Polygon in July 2022, having amassed a userbase of over 6.4 million wallets holding 9.3 million avatars. (11)

- Starbucks has launched ‘Starbucks Odyssey’, an extension to their popular loyalty program, rewarding users with NFTs. At time of writing, there has been $72k of secondary trading volume. (12)

- Meta: Facebook and Instagram have integrated NFTs, via Ethereum, Polygon, Flow, and Solana (13).

- Ernst & Young (EY) have partnered with Polygon to deploy ‘Polygon Nightfall’, an ‘Optimistic-ZK Rollup’ which facilitates private transactions and business logic.

- Nike acquired RTFKT, a crypto-native brand with one of the largest NFT communities. They are also developing a Polygon-based NFT marketplace.

Many projects are in the experimentation phase, awaiting future scalability upgrades to support user traffic of a full roll-out.

Cardano

The 4th largest NFT ecosystem by daily volume, an up-and-coming DeFi ecosystem, with a strong focus on ‘boots-on-the-ground’ adoption.

- The Ethiopian Ministry of Education and IOG are collaborating to deploy the self-sovereign identity (SSI) service ‘ATALA Prism’ to over 5 million students, 750k teachers, and 3.5k schools in Ethiopia. As of December 2022, development of the project is complete, and onboarding of students and teachers has commenced. (14)

- World Mobile, a mesh ISP operating in Tanzania with 20k daily active users. Now that the free trials are ending, customers are beginning to pay for their World Mobile connections, at half the cost of legacy ISPs. (15)

- Empowa is a ‘RealFi’ project, financing affordable housing. After financing the homes of 30 families, Empowa signed an agreement with the Municipality of Beira, Mozambique to finance an additional 25,000 climate-smart homes. (16)

- JpgStore: the largest NFT marketplace on Cardano, with ~15k daily active users/addresses and a total of 437 million ADA in trading volume (17).

- Minswap: the largest DEX on Cardano, with ~6k daily active users/addresses, and a total of 48 billion ADA in trading volume (18).

IOTA

One of the largest and oldest L1 communities in crypto, with a focus on infrastructural and governmental programs.

- European Blockchain Services Infrastructure (EBSI) — The IOTA Foundation has been working with EBSI since 2021, originally one of 7 accepted applicants in the first phase. At time of writing EBSI has narrowed it down to just IOTA and 2 other applicants (19).

- Project Alvarium — a collaboration between the Linux Foundation, Intel, Dell, and the IOTA Foundation to create a ‘Data Confidence Fabric’ for use in IoT. Recently, Project Alvarium announced its intention to work with Hedera Hashgraph, another L1 platform.

While IOTA and Hedera serve different markets: the former decentralized and permissionless, the latter centralized and permissioned, it may indicate that Alvarium is looking for more agile partners. - Zebra: a multi-national supply chain hardware and services company, incorporating IOTA into supply chain provenance (20).

- EnergieKnip: an app that incentivizes consumers to share data about their energy usage. With 30,000 active wallets, it is the largest government blockchain project in the Netherlands.

- Trademark East Africa: an initiative to streamline international trade, automating processes and cutting down on paperwork. Testing is live in Kenya, with plans to roll-out in neighbouring countries (21).

- KupKrush: a project that aims to align incentives along the recycling supply chain, specifically for used coffee cups.

- Soonaverse: an NFT-focused sidechain, with plans to eventually settle onto IOTA L1

Many of these projects are awaiting Coordicide and L1/L2 smart contract functionality, so they can finally deploy on a scalable, decentralized, and functional platform.

Obstacles, Risks to be Aware of, and Road to Mass Adoption

Ethereum

The Merge has greatly de-risked Ethereum, but much of their roadmap remains unfinished.

- Staked-ETH withdrawals are set to activate in March, in the ‘Shanghai’ hardfork.

- EIP-4844, aka ‘Proto-Danksharding’ is an upgrade to Ethereum’s ‘Data Availability’ (storage) that L2s utilize to securely settle on Ethereum L1. This is expected to arrive by Q3/Q4 of 2023.

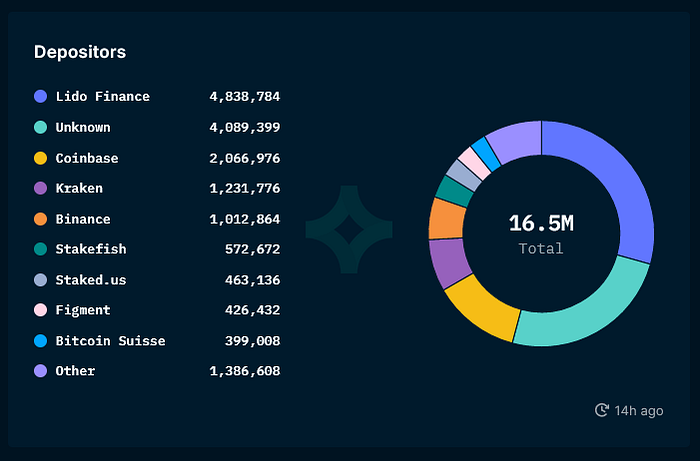

- Stake centralization and censorship: Six centralized staking providers control 11/16 million (68%) of staked ETH: Lido, Coinbase, Kraken, Binance, Stakefish, Figment, and Bitcoin Suisse, with the first 4 controlling 55% of stake (22). Not only does this threaten Ethereum’s credible neutrality, it puts the platform at risk of regulatory crackdown, given all the regulated companies running the network. 65% of Ethereum blocks over the last 30 days complied with the OFAC sanctioned addresses list, enforcing passive censorship(23).

- Inclusion Lists (or CRLists) are a proposed way to enforce censorship-resistance on Ethereum, by tracking the mempool and forcing ‘block builders’ to include transactions within a certain period. However, this still relies on an honest majority of ‘block proposers’, so it’s unclear how this will work if ETH stake centralization continues.

- DankSharding is a longer-term scalability upgrade that will build on the scaffolding of EIP-4844. Most likely to arrive in 2–3 years, given the complexity.

Long-term, the largest risk I see for Ethereum is an exodus of the biggest L2s onto their own settlement layers, secured by their respective tokens. User activity is likely to concentrate in a handful of L2s (eg: Polygon, Starkware, zkSync)

Many Ethereans would argue that L1 Data Sharding + L2s solve the Trilemma. I believe this is incorrect. While L2s do support more users, inheriting L1’s security and decentralization, if L2s are a platform’s only means to scale (as is true on Ethereum’s current roadmap), that leaves L1 vulnerable to long term economic atrophy. As L2s capture the vast majority of users, transaction activity, fee revenue, TVL, and only pay a tiny fraction to L1, Ethereum’s economic security will likely dwindle.

Sure, in a few years Ethereum could try to force L2s to pay higher settlement fees, but with what leverage? When L2 tokens capture >10x more value than $ETH, they can launch their own L1s with superior settlement guarantees, and discard Ethereum.

Of course this is highly speculative, and could turn out very differently, but in my eyes the economic incentives seem to align against Ethereum.

Cardano

With Proof of Stake (Shelley), and Smart Contracts (Goguen) live, the two pieces left for Cardano to deliver are Scalability (Basho) and Governance (Voltaire). Both of these ‘eras’ are underway, being developed in parallel, but scalability — arguably the most important — is an elusive one.

Hydra, Pipelining, Input Endorsers, Sidechains, Rollups, and L1 optimizations are Cardano’s main pathways to scalability.

A conservative version of Pipelining was delivered in the Vasil upgrade, with headroom to increase network capacity further.

- Hydra ‘heads’ (L2) are live, but other subprotocols (‘inter-head’ and ‘head-to-tail’) are necessary to support more complex use-cases (24). Development is ongoing.

- Rollups are still a while away from being viable on Cardano, primarily because it lacks sufficient Data Availability to support them.

- Input Endorsers promise to deliver on the long-awaited parallelization benefits of the (E)UTXO model, but require a significant re-design of Cardano L1. Design and specification seems likely to take another 1–2 years at the current pace.

- Cardano’s low fee revenue — a consequence of static fees and low demand — puts it in a precarious position. Ethereum L1 proves there thousands of people willing to pay higher fees for maximally-secure settlement, which flows into ETH’s economic security. Cardano must scale and fill that capacity with a large quantity of transactions to pay for long-term security.

IOTA

Stardust: an upgrade to tokenization, already launched on Shimmer, IOTA’s staging network (25)

This acts as the precursor to full L1 smart contract functionality.

- IOTA 2.0/Coordicide: the longest-awaited upgrade to decentralize the IOTA platform. Despite delays and setbacks, visible progress is being made. Optimistically, we might see IOTA 2.0 on Shimmer by the end of this year, with full Coordicide launching on IOTA by Q1/Q2 2024.

- Sidechain and L2 smart contracts are much lower-risk, there is extensive precedent to draw from in other ecosystems, it’s a matter of engineering it to fit nicely on IOTA L1.

- L1 smart contracts are more tricky, there are limited examples of UTXO-based smart contracts, and none that use leaderless consensus as IOTA does. Prototype development has begun, with an unclear timeline of delivery (26).

- The largest risk IOTA currently faces is the dwindling funds of the IOTA Foundation, who have projected 18–24 months of runway left (27). Additional funding must be found, either through investors, token price appreciation, or a second round of community donations.

Without its community and ecosystem of (prospective) builders, these factors would surely spell death for IOTA, but when there’s a will there’s a way. The Ethereum Foundation was nearly-bankrupt in 2016 (28), but through sheer force of will made it through to the finish line, and now sits on a balance sheet of multiple $billions.

In conclusion, Ethereum remains in the lead, but the same design choices that allowed it to surge ahead now hold it back from secure and scalable adoption. Cardano, IOTA, and several other platforms intend to claim the throne, each with a unique set of tradeoffs to consider.

Only time will reveal the winners of this war.

Sources:

(1) https://www.cnbc.com/2021/11/19/over-10-billion-lost-to-defi-scams-and-thefts-in-2021.html

(2) https://decrypt.co/84590/cream-finance-suffers-third-hack-losing-over-130-million

(3) https://www.theverge.com/2022/4/18/23030754/beanstalk-cryptocurrency-hack-182-million-dao-voting

(4) https://decrypt.co/98530/aku-ethereum-nft-launch-ends-with-34m-locked-in-flawed-smart-contract

(5) https://cointelegraph.com/news/bonqdao-protocol-suffers-120m-loss-after-oracle-hack

(6) https://forum.cardano.org/t/further-improvement-on-tiered-fees/106232

(7) https://docs.cardano.org/learn/eutxo-explainer

(8) https://iohk.io/en/blog/posts/2021/02/25/babel-fees/

(9) https://twitter.com/PapaGooseCrypto/status/1613973196004528128 (Cardano L1 Languages)

(10) https://usa.visa.com/solutions/crypto/auto-payments-for-self-custodial-wallets.html

(11) https://dune.com/polygon_analytics/reddit-collectible-avatars

(12) https://odysseymarket.niftygateway.com/marketplace/publisher/starbucks-odyssey

(14) https://www.youtube.com/watch?v=tHC80NFj4lo (Cardano in Africa)

(15) https://wmtscan.com/

(16) https://empowa-io.medium.com/empowa-announces-25-00-housing-project-in-mozambique-1428e356ff1c

(17) https://www.jpg.store/

(18) https://dappsoncardano.com/

(19) https://digital-strategy.ec.europa.eu/en/news/european-blockchain-pre-commercial-procurement

(20) https://developer.zebra.com/blog/getting-started-identity-enabler-zebra-iota-edge-sdk

(21) https://blog.iota.org/trademark-east-africa-and-iota-paperless-trade-with-the-tangle-aims-to-become-a-standard-in-2022/

(22) https://pro.nansen.ai/eth2-deposit-contract

(23) https://www.mevwatch.info/

(24) https://iohk.io/en/blog/posts/2020/03/26/enter-the-hydra-scaling-distributed-ledgers-the-evidence-based-way/

(25) https://blog.shimmer.network/a-deep-dive-into-stardust/

(26) https://discord.com/channels/397872799483428865/397872799483428867/1072859970879619102 (IOTA L1 SC)

(27) https://discord.com/channels/397872799483428865/397872799483428867/1051834777147277332 (Dom Treasury)

(28) https://twitter.com/peter_szilagyi/status/1334138760565559297 (EF Almost Bankrupt)

{kind=link}